February 2026 Update and the Art of Trading Less

“I miss everything about Chicago, except January and February” - Gary Cole

Alright, January is over, a short month has begun, and we’ve all certainly failed our New Years’ resolutions by now. I failed my resolution to post Monthly results after trading ends on the last day of the month instead of waiting.

So I’ll cut to the chase: I’ve got a lot of strategies running now and I’ll keep the commentary short. The trades are grouped by type to improve navigation as well. At the bottom, I wrote a small bit about trading strategy optimization that I should have figured out long ago.

-Volatility Trades (Dealing with Long/Short Vol ETFs and Options)-

Volatility Reversion Trades: [link]

Volatility Reversion conflicted a lot with the Calendar in January, unfortunately, but the 4 days that actually did trade VIXY/SVIX made $329, which is pretty good! The Volatility Reversion strategy is a consistent winner that I’ll maybe increase in position size to 15%-20% of the portfolio in the future.

Event Volatility Playbook Trades: [link]

The Event Volatility playbook did well this month, earning $279.30. I should have closed out the Thursday FOMC trades after 1-2 hours in the first day and made an extra $1000, but no one’s allowed perfect market timing. (Also, I’ve committed to consistently trading these strategies how I said I would, and work harder on not chickening out.) Still, the strategy has been doing well so far, crossing $4K in real total gains as of the end of January.

The February 2026’s Event Vol Calendar is ready and posted. FOMC-related trades will take precedence over the VIX OPEX trades, since they overlap and appear to be a stronger effect.

Monday Intraday Volatility Trades: [link]

My first SVXY trade for the Monday Intraday Vol Shorting earned me $0.90. That’s right, not $0.90 per share, but $0.90 total. Be amazed.

In all seriousness, the bid/ask spreads for SVXY were ~$0.01 when the trade happened, and Buying Market-on-Open and Selling Market-on-Close went off without a hitch, so I’m happy with what happened. We’ll see how Mondays go in the future, but this appears to be a low-stress strategy that doesn’t require quick thinking, or much thought at all.

-Intraday Option Trades (Open and Close Same Trading Day)-

Tuesday+Friday Long Call (Vibe-Traded): [link]

Vibe-traded Tuesday+Friday SPY calls had a horrible January, losing -$530. Not great, and all the losses were fast stop losses that I couldn’t really lie to myself about not closing earlier. Hopefully February is better.

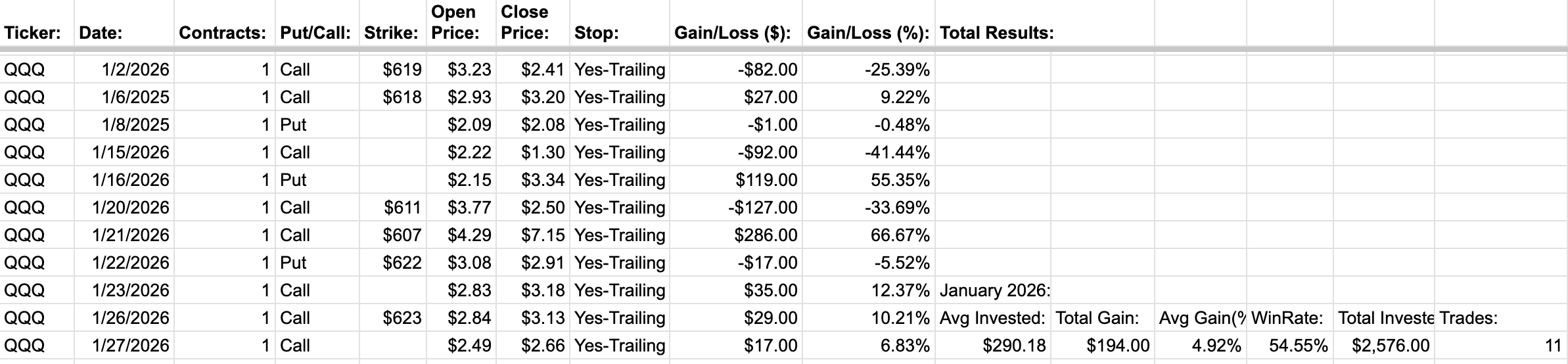

QQQ Orb Trades: [link]

The QQQ ORBs made $193 in January, across 11 trades for the month. Small gains for a lot of positions, but I was able to just let the trades happen without actively messing with them.

4-Minute SPX Trades: [link]

January had no 4-minute trades. And I still haven’t found a good “last 5-10 minutes” trade to share yet.

-Overnight Trades (Held ~1 Trading Day)-

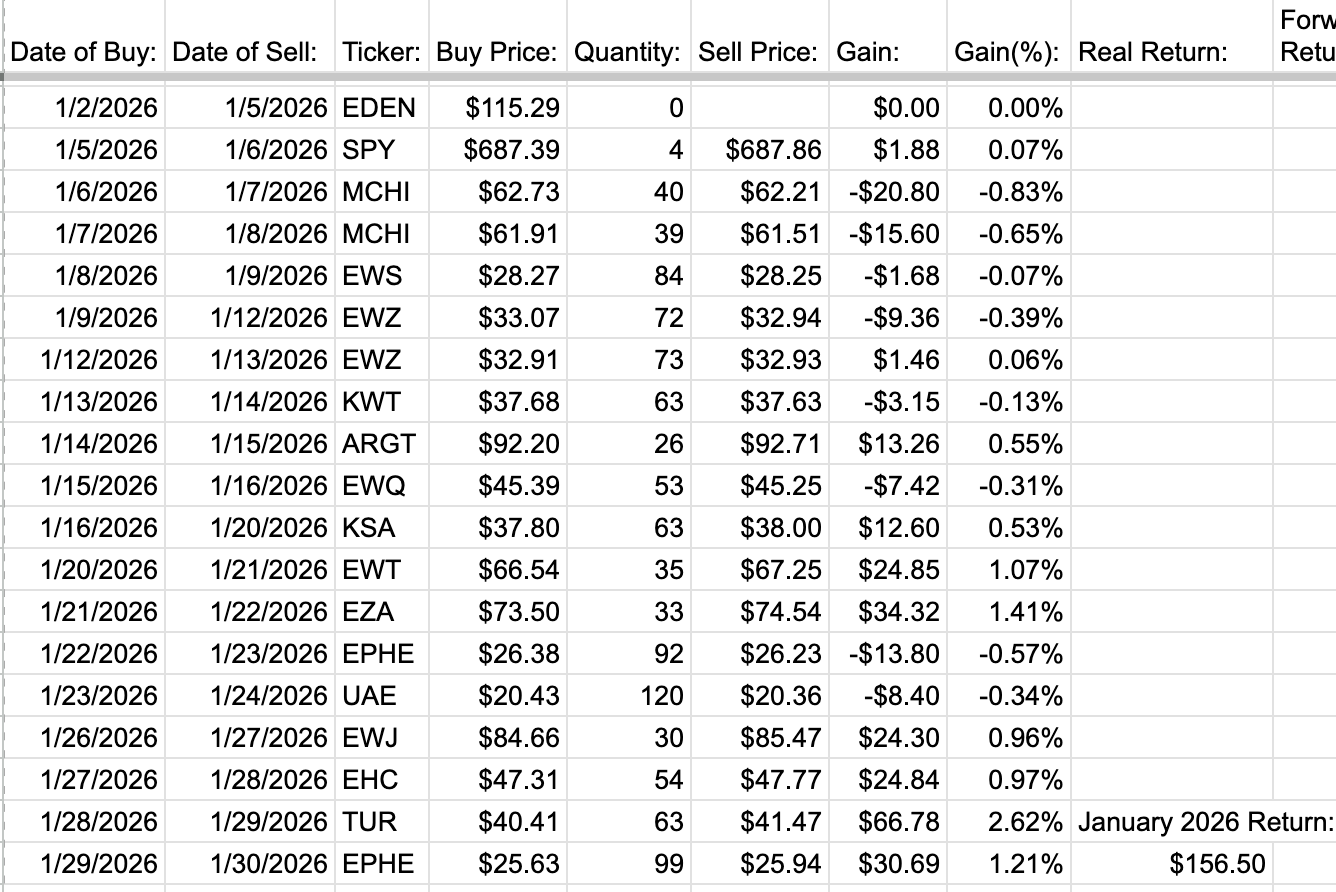

Country-Themed ETF Trades: [link]

Country-Themed ETF trades are doing well again, with a $153 gain for the month, and a rough ~2.7 Sharpe. It’s nowhere near the success of the perfectly-time hypothetical trades I’ve kept track of (which have a 3.77 Sharpe), but a 2.7 Sharpe isn’t too bad. And I’m getting better fills now that I’m opening the trades at 3:58 PM and not 3:59 PM. ( By ‘better’ I mean I’m actually opening the positions on time or after market close.)

Friday Iron Butterfly Trades: [link]

The Friday Iron Fly strategy had its first big loss this January, because I guess the President announced he was going to acquire Greenland by any means necessary and the market tanked? So on January 27th I took a max loss of -$1,149. Not great. Hopefully the strategy will recover in the future.

GLD 1DTE Trades: [link]

January 2026 returns for the 1DTE GLD trade strategy were $1,235. I’d like to think this strategy will work regardless of whether Gold goes on a generational bull run, but I’m not complaining.

-Longer Stock/Option Trades (~2+ Days)-

Emerging Markets Trades: [link]

the EDC trade was going great until the January 30th when it suffered a -$300+ loss in 1 day, but the strategy still managed to make $159 for the month of January. So that’s nice.

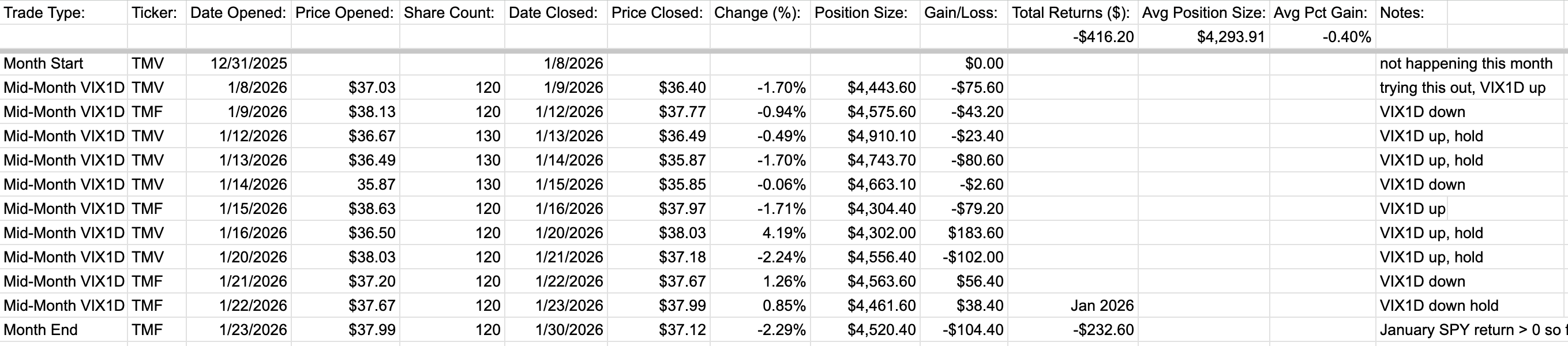

TMF/TMV Trades: [link]

TMF/TMV trades were difficult with the addition of the mid-week trading, adding up to a -$232 loss for January 2026. It was a bit frustrating to see 5+ days of losses in a row for the VIX1D-based mid-month trades, but I think that might just be part of the alpha of the strategy: be willing to endure multiple losses in a row and not tear your own hair out.

Forward Factor Calendar Spread Trades: [link]

I made a little bit more money in January 2026, working myself out of the hole I’d made at the start of this strategy with a gain of $203 over $956 in positions expiring across the month. I’m thinking that this strategy can’t be a consistent or large allocation due to the difficulty of opening more than $50-$100 of position size per day, but it’s low-stress, low-effort, and potentially profitable over the long term. I also suspect that only doing trades with 0.3-0.4+ Forward Factor levels greatly increases the profitability, but this will take time.

The Art of Trading Less:

Now that the review is over, I’ve got a small tidbit to cover.

Oftentimes when I make a strategy and feel great about it, I find out later systematically reducing the number of trades it took would have made it more profitable.

For instance:

The TMF/TMV trade works better when SPY’s return month-to-date > 0, instead of every month.

SVXY is a great long on Intraday Mondays, and holding until Tuesday when SPY’s Monday return < 0 improves the results to better than buying and holding.

What was an attempt at trading 1-day SPX options overnight became an Iron Butterfly on SPY that works best on the Friday-Monday expiration cadence when SPY’s price is above a 10-EMA.

Short Volatility trades trades often do better when VIX < VIX3M at market close.

These kinds of rules weren’t found easily, but I think if I can just do multiple simple strategies that overlap in a timeframe, they can replicate one giant algorithm that’s supposed to be fine-tuned, perfect and one-size-fits-all. (That single algorithm would likely be overfit and fragile anyway.)

So I figured while I’ve got some space to write them, I’d just add some things I’ve noticed to prior trading strategies, but didn’t have a good time/place to mention before.

For the EDC trades, the Sharpe and profitability greatly improves when the Friday afternoon-Monday afternoon holding time is eliminated.

For the FXI China trade, the same no-weekends improvement holds true fas well. In fact, the reduction in days traded boosts the Sharpe Ratio for the strategy up to a little over 0.92 with very little loss in overall returns, which might make it viable using 3X leveraged ETFs. I’d have to check trading it myself to see if the bid/ask spread isn’t too bad.

For the GLD trade, historically, most of the profits happened on the Thursday-Friday 1DTE option cadence. Limiting the trade to once per week greatly enhances the profit factor and Sharpe, even before GLD’s bull run.

If you guys can find simple trading limitations on a strategy I’ve posted, or limitations for strategies you made yourself, I’m all ears.

Stay warm, and happy trading.

- Lay Quant

Have you looked into sizing the gold trade? Assign one point for the spy criterion, one for Gld, one for vix and one for Friday and then buy 0-4 contacts (or whatever size works).

Thanks, what a curious list of strategies, mostly seasonal/calendar. Do you also trade stuff like VRP-harvesting, or other short-vol type of strats?