March 2026 Update and Some ORB Alternates

“In March I’ll be rested and caught up and human.” -Sylvia Plath

Hi all, the trade updates are getting longer, so I’ll try and make the commentary shorter this time as the entire market seizes up from a new war in the Middle East. Let’s first go over February’s results, organized by trade type just like last time. Then, I’ve got a quick expansion to the ORB trades to share, because the QQQ Long Option ORB trades have been causing me stress from their return distribution.

-Volatility Trades (Long/Short Vol ETFs and Options)-

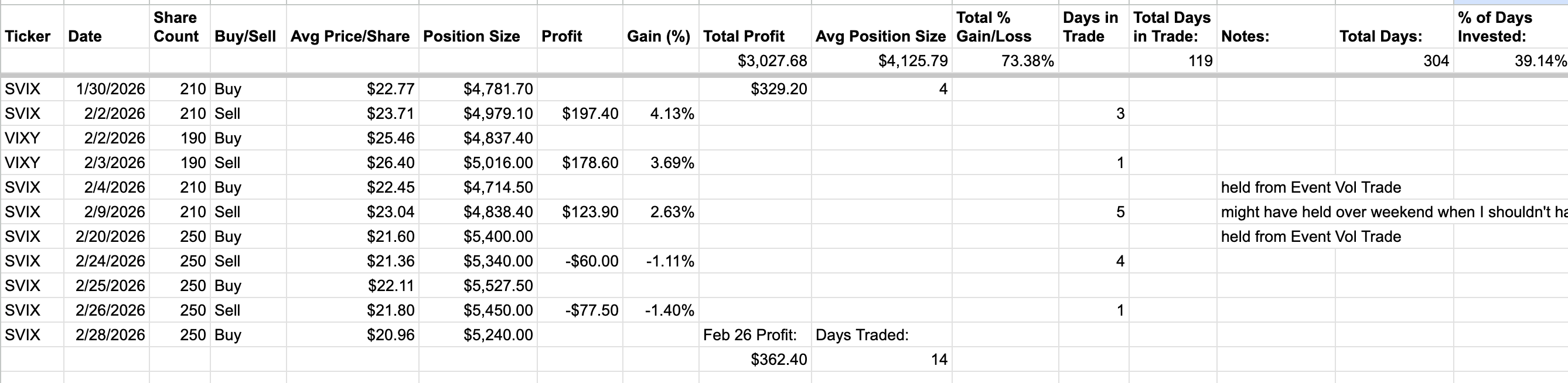

Volatility Reversion: [link]

Volatility Reversion did well for February earning $362.40, with most of the gains in the first two weeks of the month. It’s still working, and I’m still happy with it. Judging by the results and readership metrics it’s my most successful and popular strategy. Some of the positions were held over from the Event Volatility Playbook to avoid double-counting, as noted in the images posted.

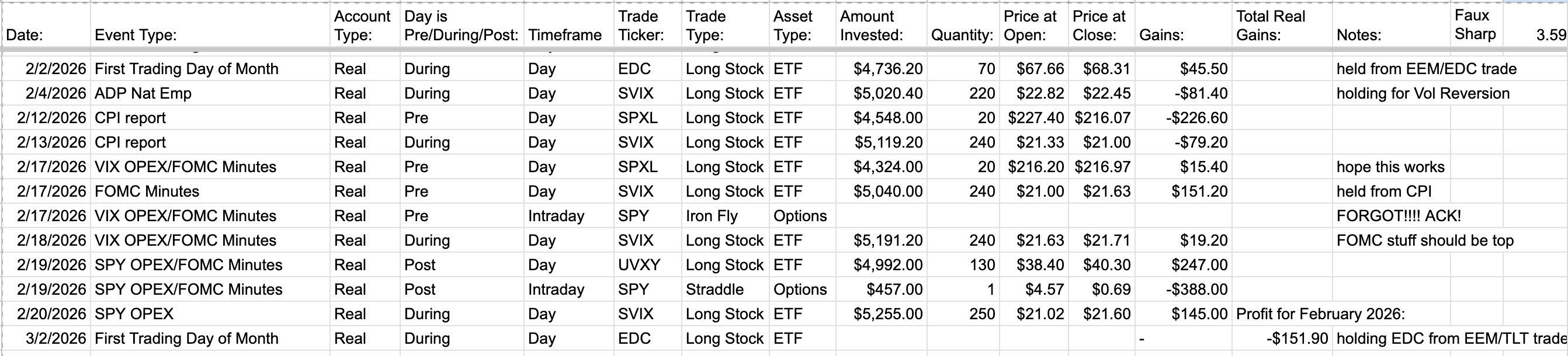

Event Volatility Playbook Trades: [link]

February 2026 saw the first loss for the Event Volatility Playbook, losing -$151.90 for the month. Most of the pain came from the SPY 0DTE OPEX straddle on 2/19.

March’s 2026’s Event Vol Calendar is ready and posted, as well.

Monday Intraday Volatility Trades: [link]

Total Monday Intraday returns for February were $167.50 across 3 trades. Now with a few trades under the belt, I can say this strategy is working well, especially with the ‘hold-to-Tuesday’ variant. The 2/23 trade ended Monday with a $100+ loss, but after holding until Tuesday it closed out with a $1 gain. I’m having no issues with fills using Market on Open or Market on Close orders so far.

-Intraday Option Trades (Open and Close Same Trading Day)-

Tuesday+Friday Long Call (Vibe-Traded): [link]

The Vibed SPY Long Calls lost -$20 in total for February across 3 trades. I didn’t get much chance to take gains and run for the 2 losing trades, since SPY immediately tanked after I opened them.

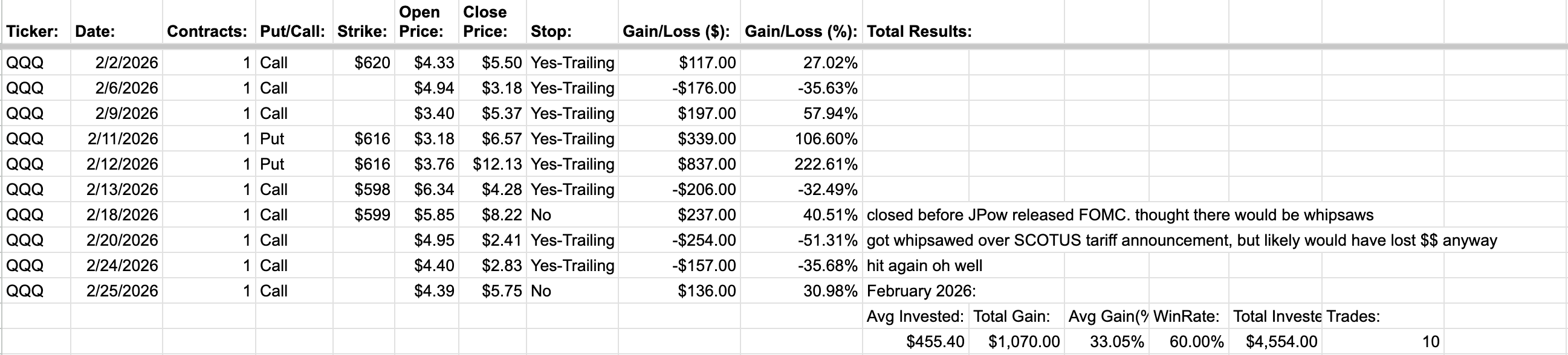

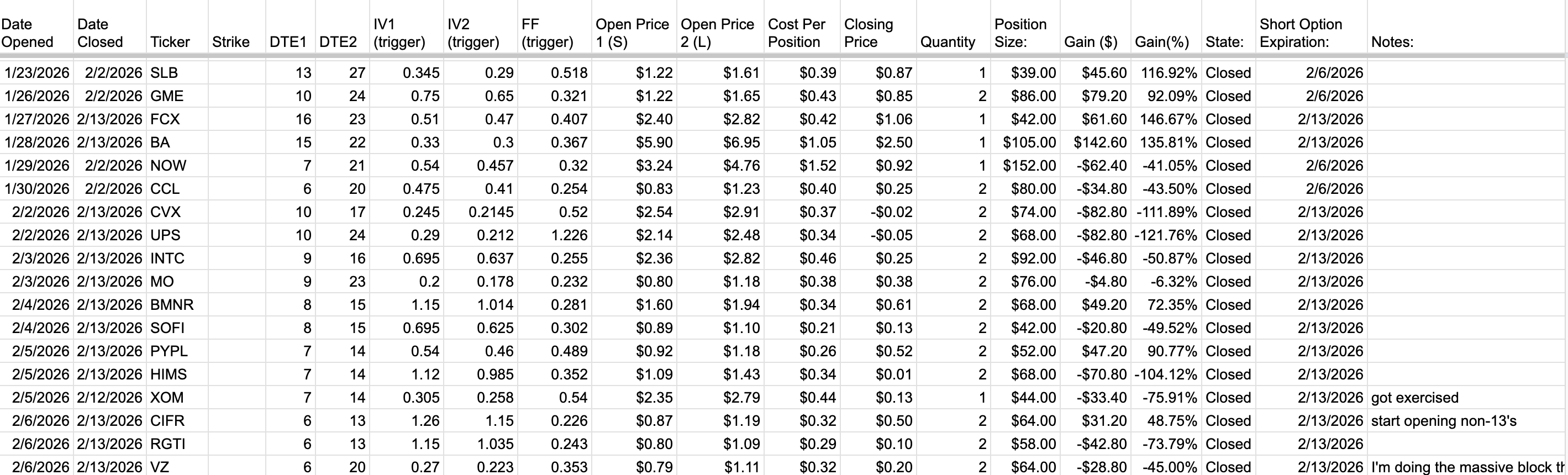

QQQ Orb Trading: [link]

The QQQ ORBs made $1,070 in February, across 10 trades for the month, a really pleasant surprise. Most of the gains were from the 2/11, and 2/12 trading days, which made the following losses a bit stressful as profits got chipped away.

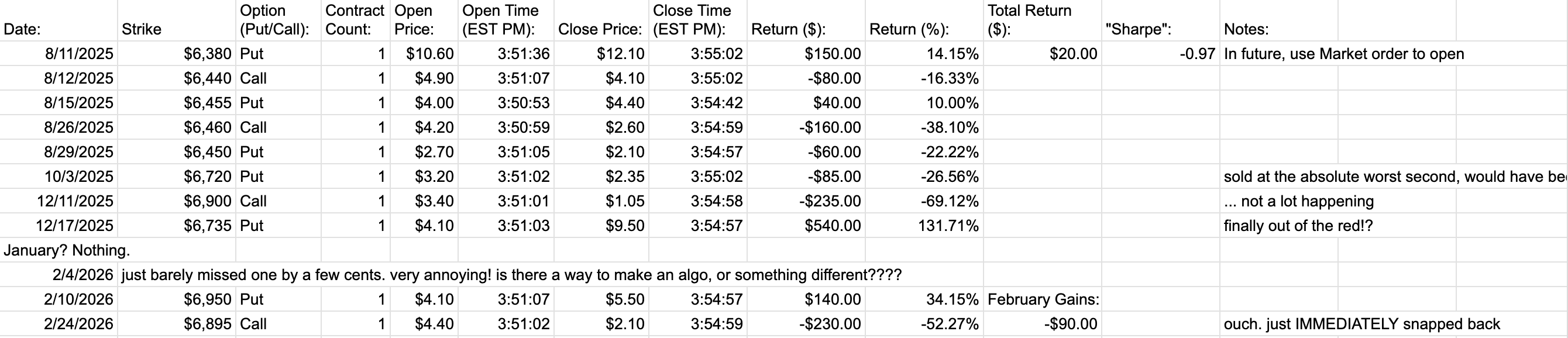

4-Minute SPX Trade: [link]

February had two 4-minute trades that lost -$90 in total, as well as one missed trade on 2/4 (that would have made money) that I didn’t open because it didn’t pass from an eyeball check, but did by about 20-30 cents when I did the math at the end of the day, likely costing me $300-$500 in missed profits. Frustrating.

-Overnight Trades (Held 1 Trading Day)-

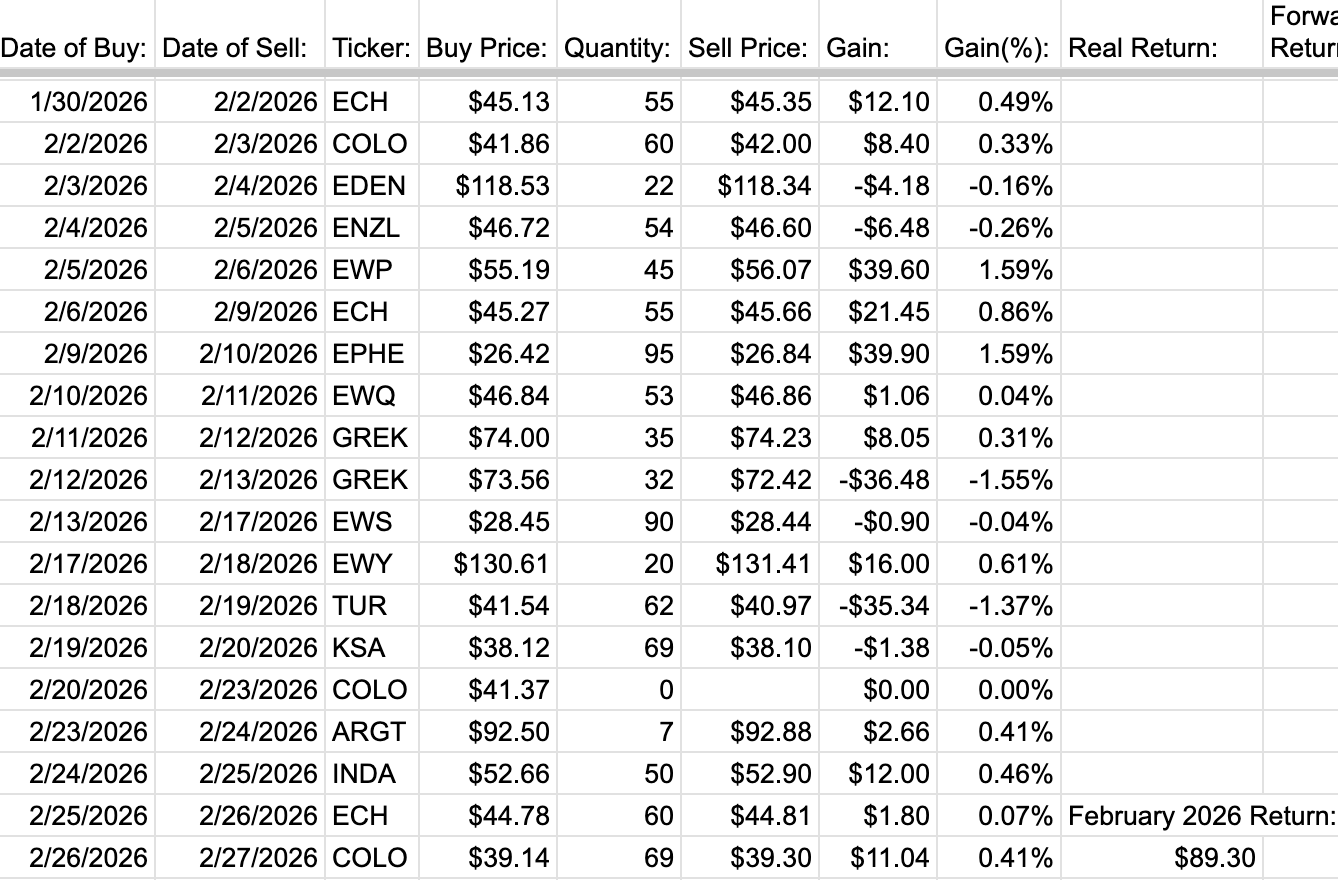

Country-Themed ETF Trade: [link]

Country-Themed ETF trades are doing well again, with a $89.30 gain for the month, and a roughly ~2.93 Sharpe overall.

Friday Iron Butterfly Trade: [link]

The Friday Iron Fly strategy lost -$153.00 total in February in two trades. The 2/23 trade had to be manually entered because of some algo issue, but I was able to open it in the last 60 seconds of trading on Friday, even though it led to a big loss. I’m a little worried this trade won’t last when I heard the news that Options and Stock trading will soon ( in May 2026?) be 24/7.

GLD 1DTE trades: [link]

January 2026 returns for the 1DTE GLD trade strategy were $1235 for 2 trades. In both trades I chickened out and sold early, but it might have been for the best, as GLD ended down for the day, and the option would have likely triggered at a 50% stop loss. If GLD stays volatile, I may have to revisit the GLD 1% cap I’d made for the original test. It seems that +/-1% days are becoming normal.

-Longer Stock/Option Trades-

Emerging Markets Trades: [link]

The EDC system has recovered from the $300 January loss, making $964.60 in profits for the month of February. I have 70 shares of EDC currently open, and the trade position will be shared with the Event Calendar’s ‘First day of the month’ trade.

TMF/TMV Trades: [link]

TMF/TMV were profitable for February, earning $297.40. SPY was down for the month for both the February Month-end and the March Month start, so the system won’t hold TMF/TMV until 3/6/2026, and all February gains were from the VIX1D mid-month trades. I didn’t actually think it would be profitable immediately, but I’ll take the win.

Forward Factor Calendar Spreads: [link]

I made $490.80 on the Forward Factor trades in February, largely because of a lucky break with SHEL where the day before the short option expired, it got exercised, and then I covered the short shares 81 cents below the original call strike. Assuming my luck continues, this is a decent system making about 20-25% per month on a small base of capital with minimal management. If trends continue, this system will be profitable by the end of march. Also, it seems that megacap stocks like AAPL have Monday-Wednesday-Friday options, which seem to work okay with Forward Factors.

Commodity Calendar Trade: [link]

The Commodity Calendar trade is up and running, and is moving from UGA February to UTSL March. The system made $368 in February, holding UGA for a total of 16 calendar days. I have a UTSL position open as of February 27th, and will be holding UTSL positions when the VIX move is > 0 at EOD.

Opening Range Breakout (ORB) Alternatives

As I was dealing with the emotional highs and lows of the QQQ ORB trades, I wondered if there was a way to mute the pain a bit. The way the strategy works currently is that it has a bunch of small losses, and a couple of big wins that (hopefully) balance it out as a good profit.

What if there’s another way to profit from 0DTE options for intraday breakouts?

I fiddled a bit with OptionAlpha again and found that 1-hour breakouts work pretty well for Credit Spreads. And tehy have the opposite return structure of the QQQ ORB strategy: A lot of small wins, a few big losses. A good sweet spot seems to be 5-30 Deltas for the long/short option strike positions, and no stop losses. A 95% take profit feels okay, because fretting over 2-3 cents for a position seems a bit much, and by the time the position is that deep in profit, there might be a lack of bids for the far-out 5-Delta leg.

I assume that this trade works because like several different trades I’ve outlined like the Weekend Iron Fly, we’re selling expensive risk premium against a beginning intraday trend.

I found this strategy works pretty okay for multiple 0DTE option backtests on SPY, QQQ, IWM, GLD, and even TLT, (OptionAlpha backtests Linked by Ticker) if you ignore FOMC days. I’m leaving out FOMC days here because of volatility compression until the announcement, and then frequent whipsaw behavior. Profitability for these spreads can be increased by adding maybe 1 more basic filter to the trade like IV Rank, EMA-10 over/under, or VIX movement for the day, which I think is reasonable. At the moment, I’m just doing QQQ and IWM, and can include them in the monthly reviews upon request. Although QQQ and IWM have decent fills, I suspect that GLD or TLT would be more difficult positions to open from the historically wide bid/ask spreads. And SPY ORBs would likely interfere with the Long calls and Friday Iron Flies.

Thanks,

Lay Quant

I always have fun reading. Articles are with great insight.

Thanks, do you modify/mute your strategies during stressing periods like this one (Iran war)?