Trading Options on GLD

[Gold] gets dug out of the ground in Africa, or someplace. Then we melt it down, dig another hole, bury it again and pay people to stand around guarding it …Anyone watching from Mars would be scratching their head. ― Warren Buffett

This one will be short and simple. It’s the holidays, so no one wants to spend an hour reading a long post with complicated theory and code.

You know how everyone’s talking about gold lately? Buying gold, mining gold, beating the Federal Reserve, gold’s going up, digital gold, blah blah. Gold Standard this, Gold Standard that.

Personally, I don’t care about it. Even if I' did, I’m not a good macro trader in the first place. I just want money at the end of an investment to be more than what I started with, whatever the denomination it is.

Background on Gold

About a year ago, a friend told me that I should buy gold (physical) and hold onto it. I and other friends laughed at him, but it’s up about 70%+ since then and he’s calling me poor every chance he gets.

Anyway.

Gold acts weird as an asset, with a 0-0.3 correlation with the overall US stock market. It’s used in Electronics, Jewelry, hedging, diversification, hoarding, and probably some other stuff.

One of the first twitter posters that got me interested in Quantitative Trading wrote two posts about Gold, one of which I’m still looking for in my notes.

The second Tweet was something to the tune of: “You can replicate ~100% of GLD’s return by only holding GLD the trading day after SPY had a positive 1-day return.”

At first I laughed it all off. But then I thought, “well, it can’t be that hard to test?”

Backtesting on Gold

So I quickly spun up a backtest with yfinance data dating as far back as possible.

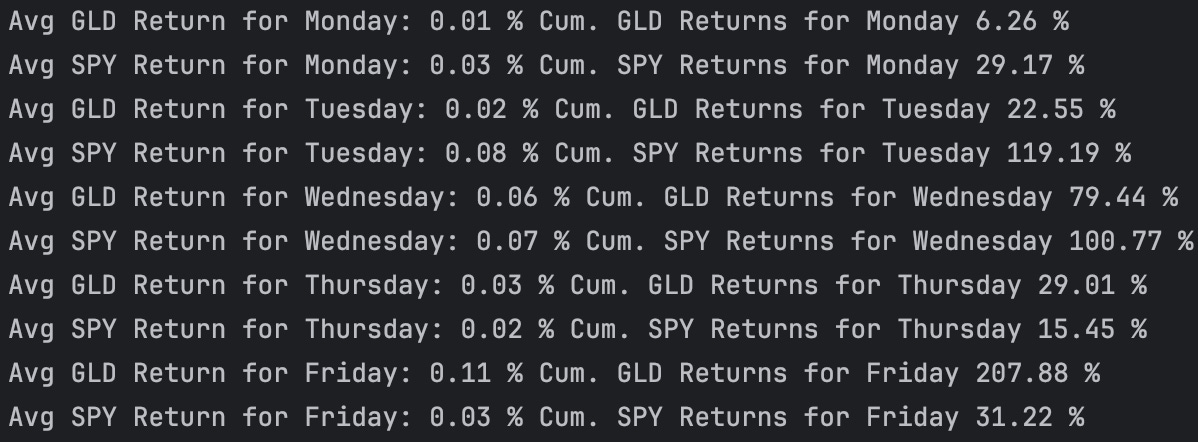

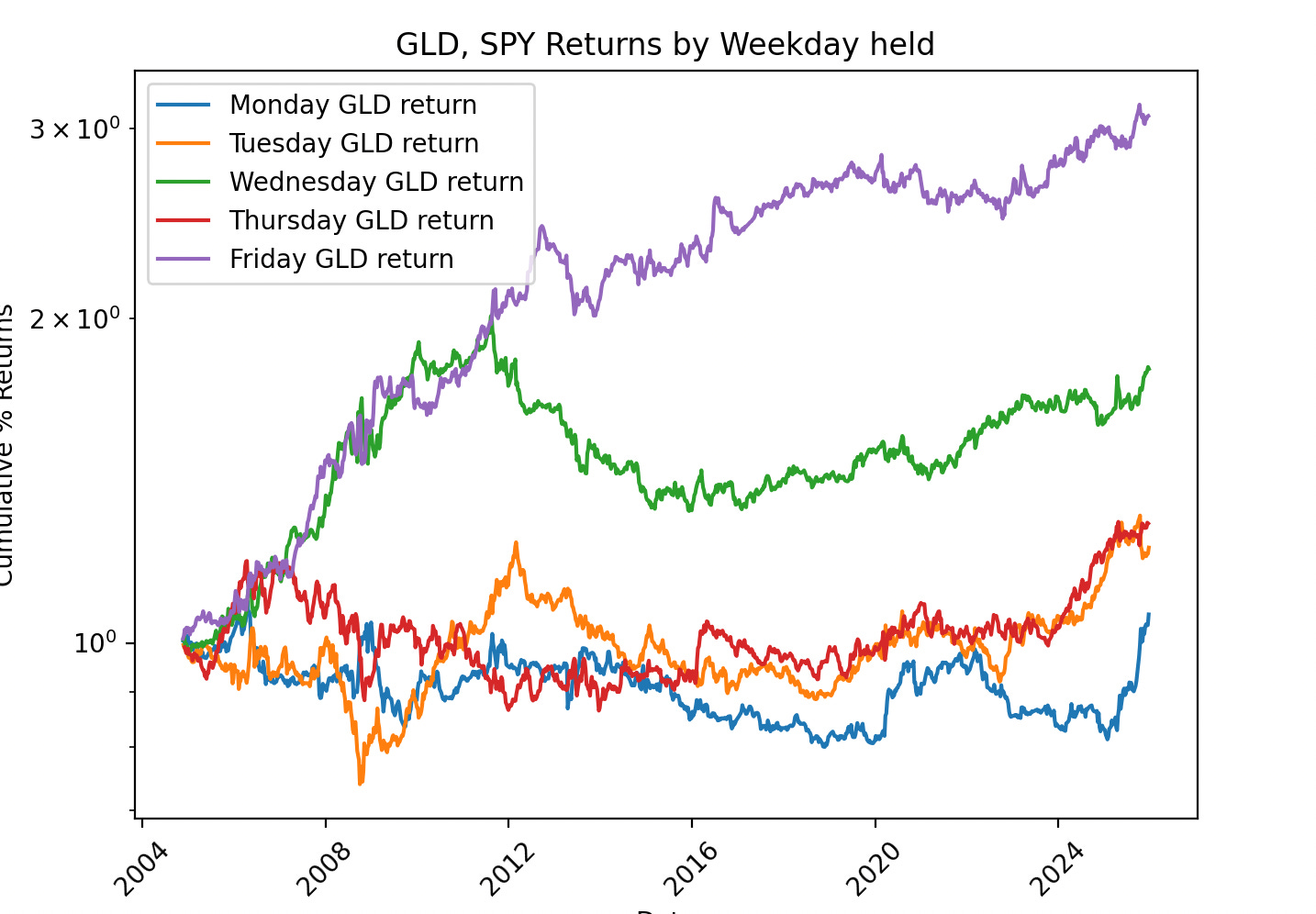

And infinitebid.exe was right about Fridays! +0.11% Average return per Friday is pretty big.

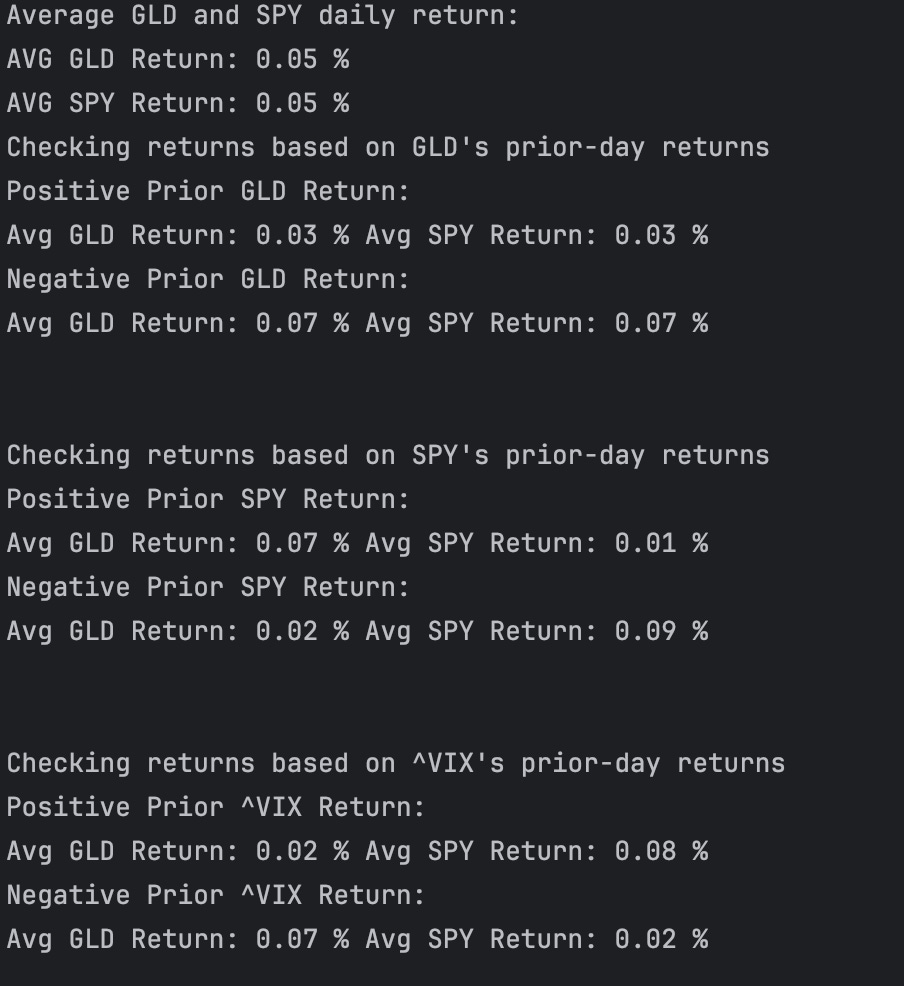

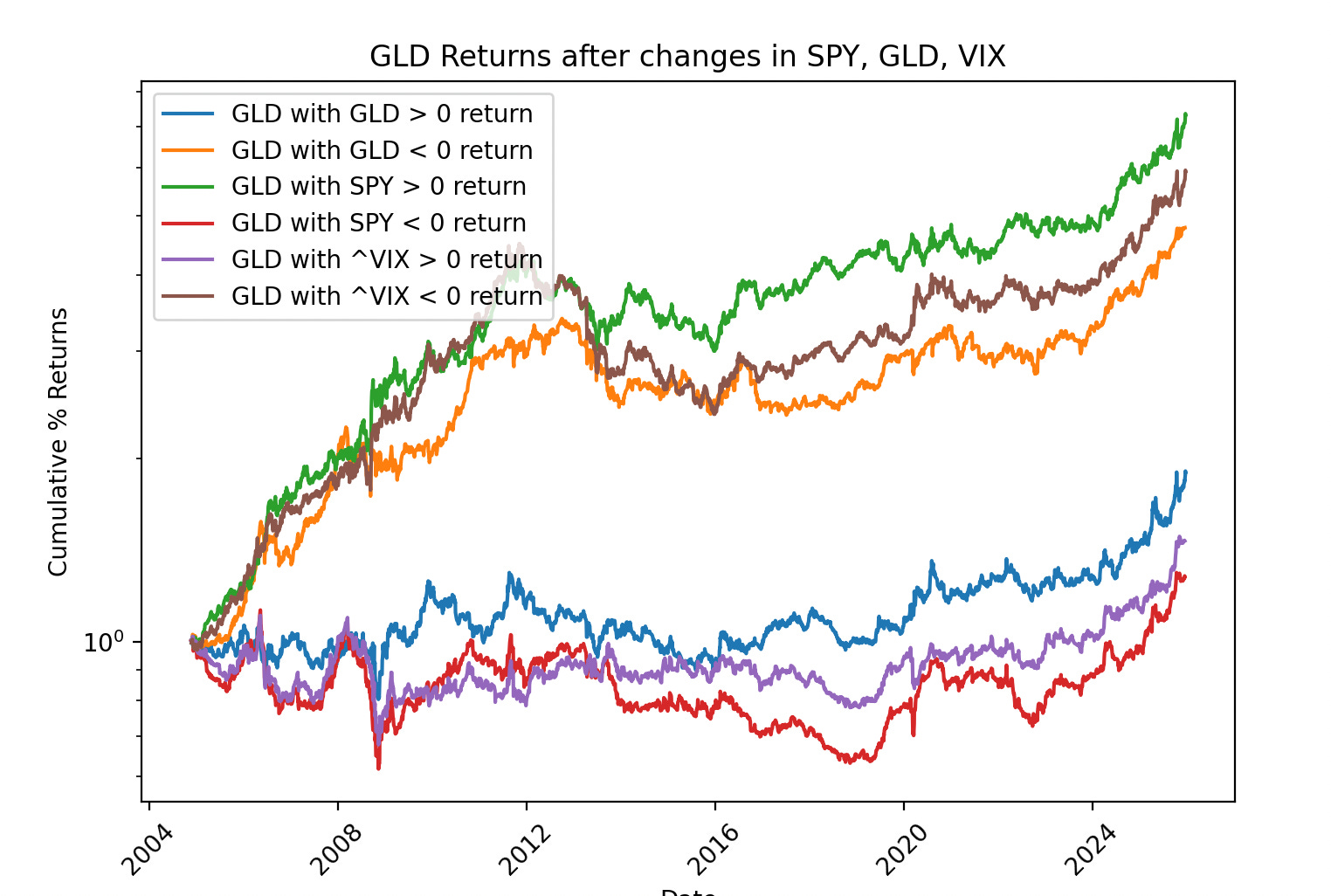

If we also look at the positive/negative prior returns for SPY/GLD/VIX also work, we see a pattern too. VIX down, GLD down, and SPY up are good for GLD returns.

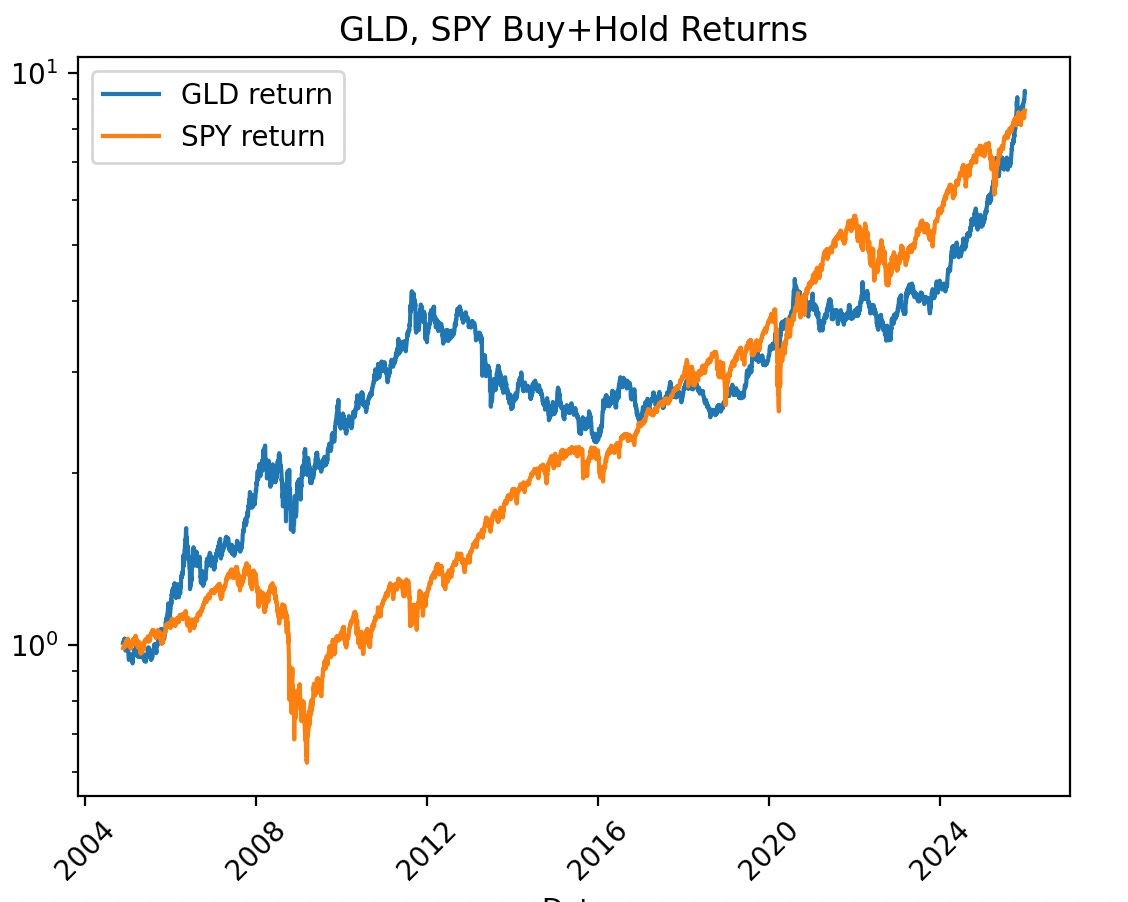

The log-scaled long-term buy+hold returns for Gold (GLD) and the market (SPY) look like this since 2006:

And it turns out you can cut your needed exposure to Gold in half by just holding GLD on trading days after SPY has gone up, or at least not down too much. (It’s probably a rebalancing move, not that I can really prove it.)

Also, it seems that Thursday nights to Friday nights historically have been one of the best days to hold gold. Possibly because jewelry or investment firms all buy on Friday?

Actual Trading on Gold

But sub-15% annual return on capital per year just using the underlying stock isn’t sexy, and I’m too chicken to trade futures. So how do I take advantage of this anomaly in a really profitable way?

Let’s go back to options. Glorious, glorious 1DTE options. I think best ETF for messing with gold is likely GLD, since there are now 3 GLD option expirations per week. [Mondays, Wednesdays, and Fridays]

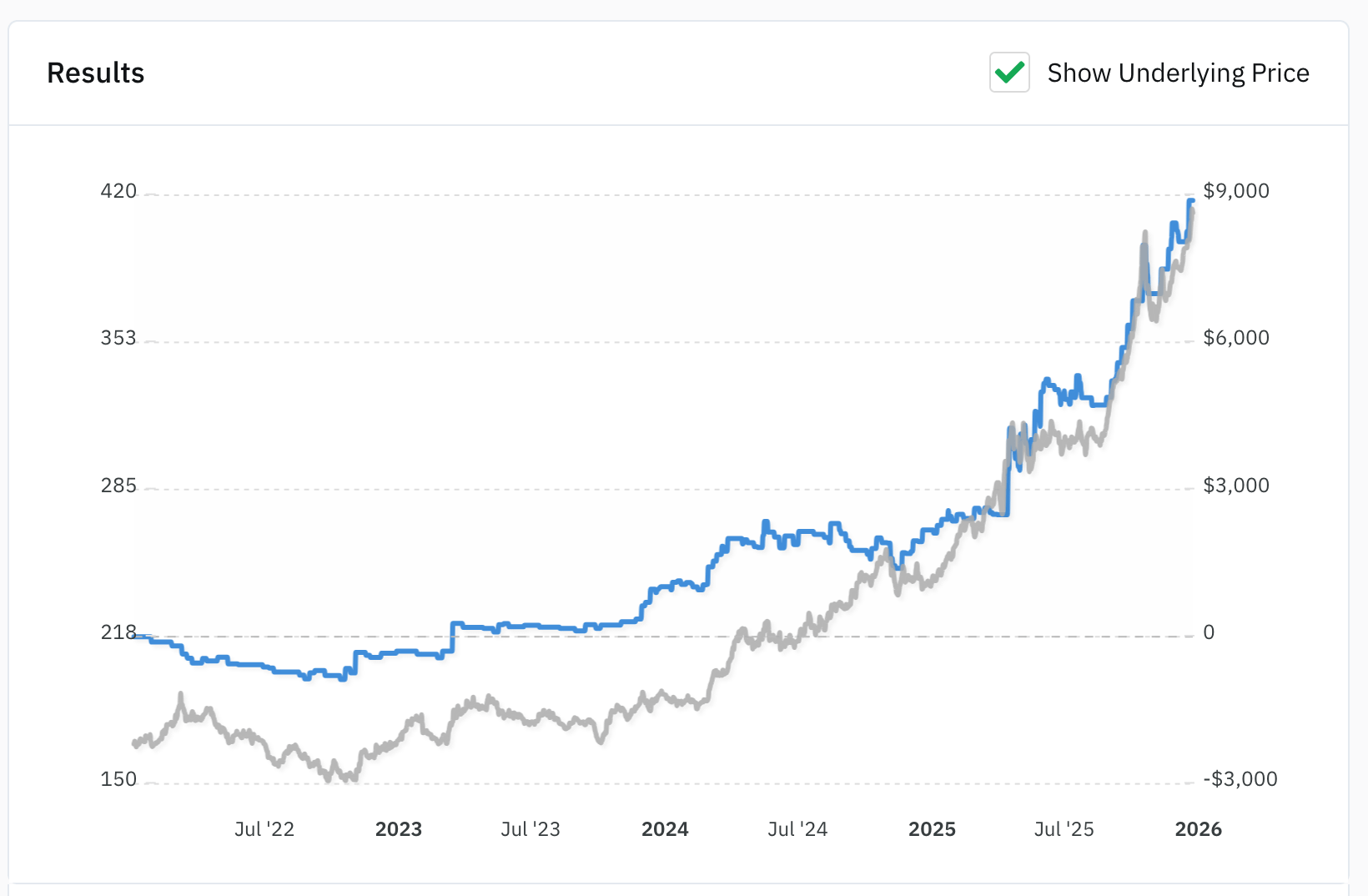

With an OptionAlpha automation, we can check for trade conditions in a second at 3:55PM and then buy a 1DTE GLD option. And with Backtests, we can see if trading these options was generally a good idea in the first place since 2022. I made this backtest in OptionAlpha a few months ago fiddling with the idea. Really simple rules. 50% stop loss, if possible, VIX is dropping, GLD’s prior day move was below 1%… It might change in the future if I decide to use a different combo of GLD/SPY/VIX rules, but the results should be similar.

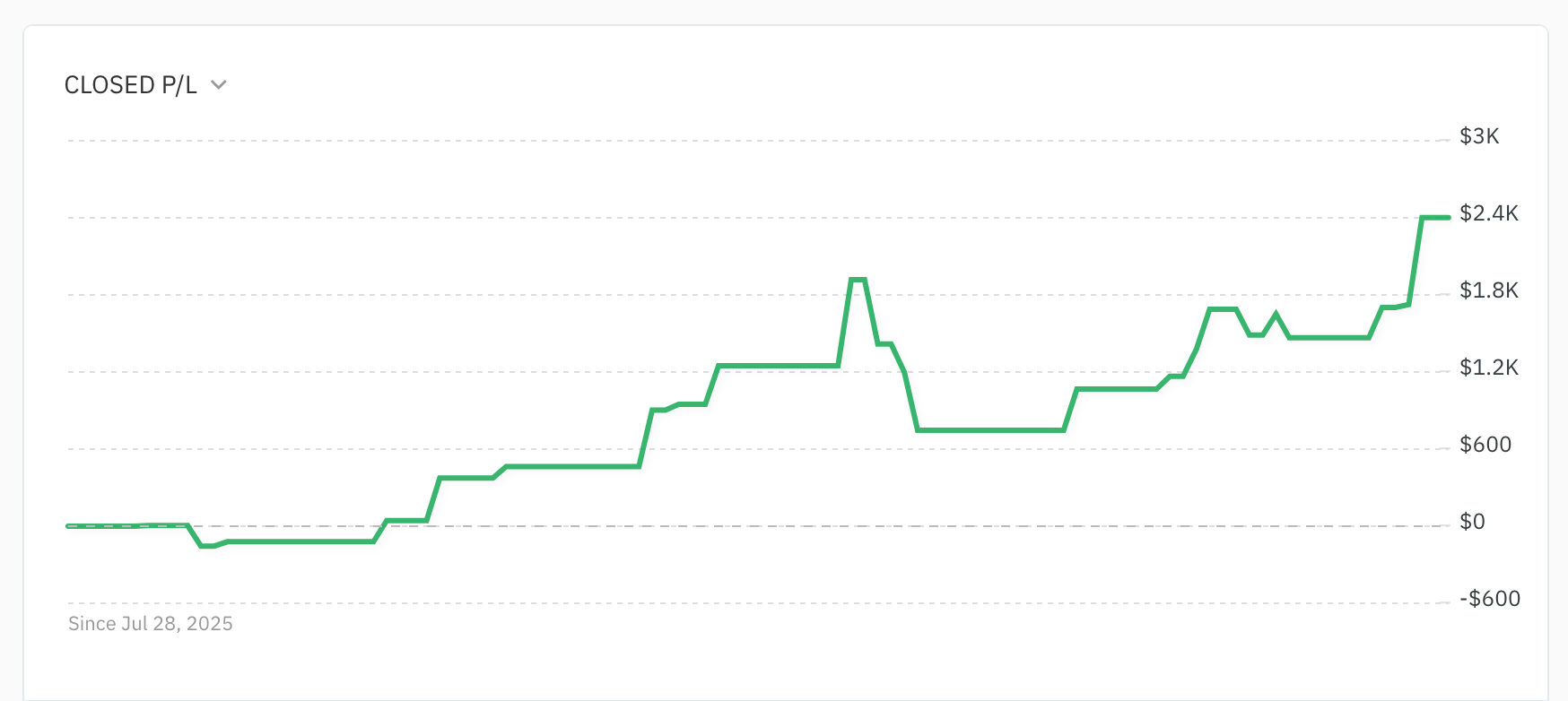

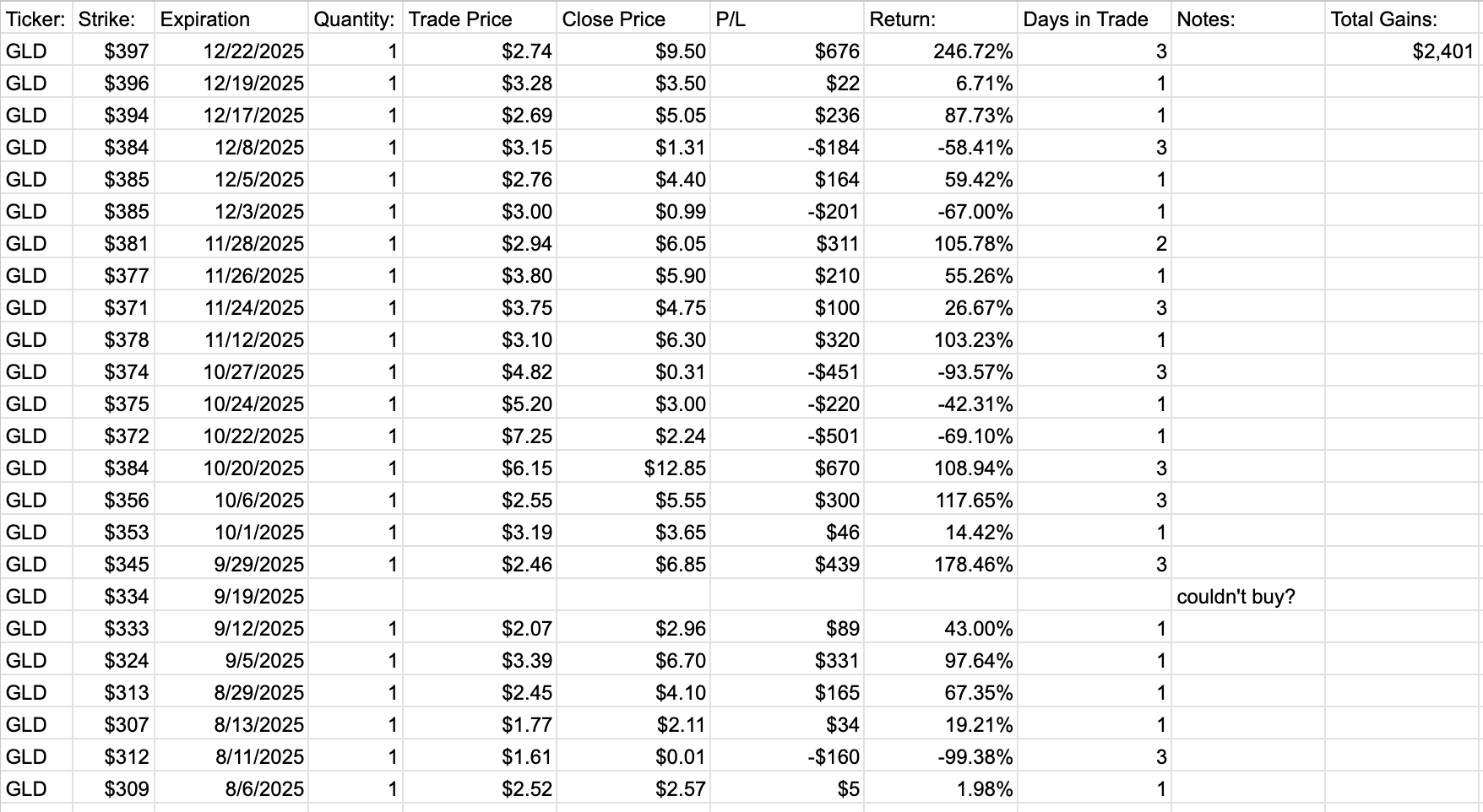

The backtest results look like this trading on 1 contract at a time:

At a ~0.7 Delta (decently in the money), you are often 50-100x leveraged. For a 1-day trade. And if GLD drops 10% (>$40 per GLD share at this point) your position won’t get blown out like with. In the backtest, a majority of the returns came from Thursday close to Friday close moves. So a trader trying to maximize the average profitability of the trade could just trade once a week tops.

Also, importantly, because it’s a 0.7-Delta Call, there’s very little extrinsic value in the Long Call option. If GLD is up 0.05%-0.10% at the end of the day, the option will likely be profitable or breakeven. A 1%-2% move is a 100%-200+% gain for the option.

Now, I’ve been trading this using OptionAlpha (and automatic stop losses at -50% loss, along with a bit of ‘vibe’ closes on trades I think will move against me. As usual, it might be better in the long run to just stick with the original plan, but I’m far from perfect.)

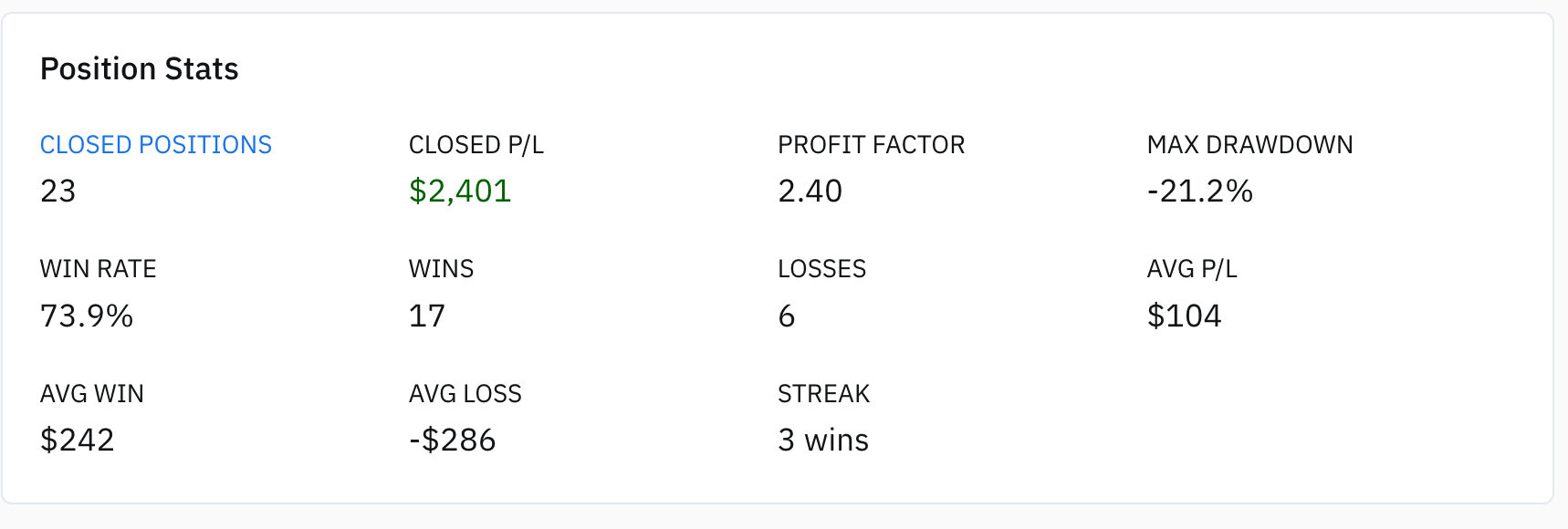

And the results have not been bad at all.

~2.4 Profit Factor for the trades, Sharpe (according to OptionAlpha) above 3 so far. And a small outlay per contract of only $200-$500 in order to control $40K-worth of stock. Not Bad!

The results below include me panicking and selling too early a bunch of times based on the “vibe”, so while these are my personal trades, they’re probably not the optimal profits and losses.

Future ideas could include:

Refinement of the entry conditions.

Adding 2DTE trades for Tuesday+Thursday moves to improve from a 3-day to 5-day strategy.

Spread trades of some sort for the days this trade doesn’t trigger? A bearish GLD strategy

I’ll add this GLD 1DTE Option trade to the monthly updates going forward.

Here’s a link to the code for the GLD backtests and EDAs, and Happy Holidays.

Lay Quant

Shocking how simple strategies like this one work so well...ever tried to go long bonds at the end of the month and short at the beginning?