Trading options on the VIX Index itself

So I'm always on the hunt for more trading ideas, especially simple ones that won’t violate PDT rules or require monitoring. The VIX-VVIX-SPY option trades are currently causing me some frustration, but that’ll be explained in the October 1st update.

Anyway.

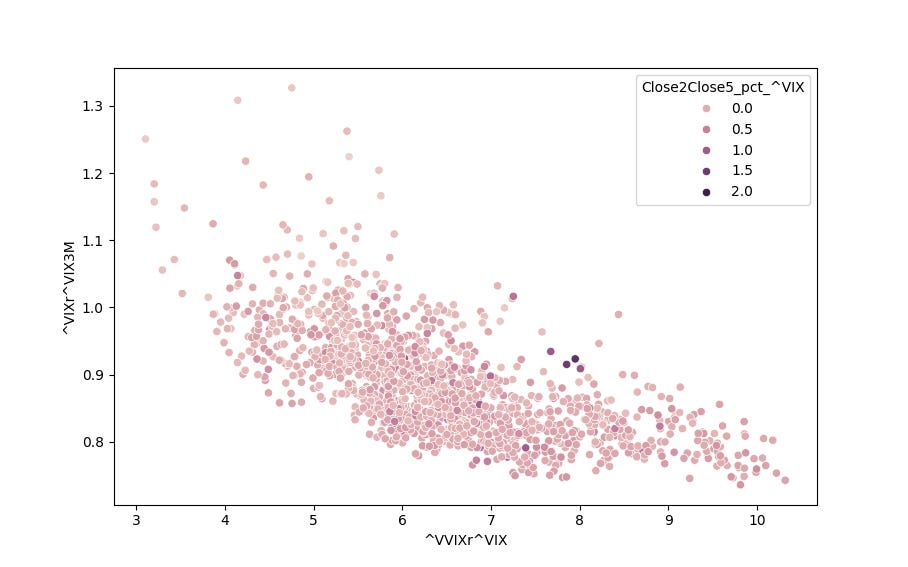

I recently saw this study that looked into VVIX and VIX ratios. Feeling a little inspired, I tinkered with ratios and Volatility indexes and found that there can be a bit of a sweet spot in daily closing data, based around 2 rules:

1. VVIX / VIX < 6. Meaning that there isn't a large difference between SPY's Volatility and VIX's volatility.

2. VIX / VIX3M between 0.9 and 1.5. Meaning that VIX is close to or in Backwardation. (Backwardation means that a near-term derivatives contract is more expensive than a longer-term contract, often in futures contracts. Think of it as an inverted yield curve, but for Volatility readings.)

I noticed that when our data is in the region mentioned above, the VIX drops pretty heavily the next few days. Around 65% of the time the VIX Index is negative at the end of 3 to 5 trading days, compared to around 55% in normal periods.

So I created some code to simulate trading VIX options to find an optimal strategy to tke advantage of this given the past 2 years of data. I checked a couple variations of option trade types with this trade, from Long Calls to Iron Butterflies.

The below chart gives results for opening one of the option strategies on the VIX with at least 5 DTE every day, then closing the trade on the Open of the last day.

And the below chart shows the results of opening these strategies when the VIX is at the parameters outlined. (Note that the VIX itself cannot be directly invested in, although an instrument like VXX or VIXY could be held as a long equity position instead.)

It turns out that VIX Credit Call Spreads (Write a Call at the At-The-Money Strike, and Buy a Call $2 Out-of-The-Money) are effective, with an Expected Value per trade of $12, 184 trades completed, and total profits of approximately $2200 in our 2 years of trading. We can see from both results that selling a straddle or short call strategy would make more money, but the margin requirement and inherent risk of a short call position is so massive I’m not willing to try it myself. Note how last month there was a $5K drop in the regular straddle trade during the small “Volmaggedon“ after the Japanese Carry trade imploded, while the Credit Call Spread strategy barely dropped.

My guess as to why this consistently makes money is because a lot of institutions and traders buy VIX options to hedge, but they aren't very picky about the price. So there should be long-term profit to be found in taking the other side and selling them that protection. An elevated Volatility tends to drop over time, and with a call credit spread, the strategy would also make money from theta (time) decay.

Since we're not using expiration dates longer than 1 day, there's an additional wrinkle to how risk and reward for the strategy works. The amount of capital required across a week can vary, since the trade can be triggered 4-5 times before the earliest open VIX position expires. It’s possible you could be required to have margin to keep 5 successive VIX spread trades up at once, opening a new trade each day from Monday to Friday.

As usual, I expect that trades in theory will be very different to how they operate in practice, and so I'll start using this strategy in October. I’ll also refactor the code soon so it can more easily analyze other strategies and underlying assets besides the VIX.

Code can be found here.

- Lay Quant