A July Update and Another Strategy Revisit

"One of my advisors will be an average five-year-old child. Any flaws in my plan that he is able to spot will be corrected before implementation." - The Evil Overlord List

So, a rather volatile month has concluded and we're all still alive, right? Wonderful! Let’s take a look at how trading has gone in June.

July Strategy Update:

Volatility Reversion:

This strategy is the first one posted since returning from hiatus, and it’s doing great. Pretty much every trade has made money from open to close. The total earned for the month of June 2025 was $422.98 on approximately $3,300-sized positions.

I'm tempted to double the position sizing to 20% (to a half-Kelly bet), but I’m still adding and modifying strategies that might be heavily correlated to this one.

Emerging Markets:

This strategy is a net-zero outlay long/short ETF strategy switching between EEM and TLT longs and shorts based on relative SPY/TLT 1-day performance.

The strategy is currently unprofitable and difficult to trade. I don’t mind the current unprofitability, since a walk-forward of the backtest I posted shows roughly the same returns.

What I do mind is that I'm missing too many short EEM trades (at least 3+ within 20 trading days) because of EEM sometimes being "hard to borrow" and I can’t resolve it with my broker fast enough in the last 5 minutes of trading. This makes the long-short strategy no longer worth pursuing, since I’ve been trying to open short positions the next day in the morning, or in after hours trading, if they can be opened at all.

Closing a long/short, and then opening another long/short each day is frustrating and causing some slippage. With my broker and account size, a 13% borrow rate also isn't ideal for a strategy that will be short something every trading day.

So we’re switching to Long-only EDC trades. As listed in the EEM article, this trade is simple. Open a 10% position on EDC when SPY 1-day return < TLT 1-day return at market close. The Sharpe and drawdowns are not the best for this strategy when backtested like it’s traded full-portfolio, but as a much smaller position with rebalancing and other strategies alongside it, it shouldn’t be too bad.

QQQ Opening Range Breakout (ORB) trader:

The ORB trade was detailed in this post. I’m doing an automated 5-minute Opening Range Breakout on the QQQ ETF when the VIX index has negative returns since the prior close.

It’s still way too early to tell whether QQQ ORB works, but I’m not dissatisfied. The fills are reasonably fast entering and exiting QQQ options. Here are the results so far:

It’s possible that a no-stop-loss ORB might be better in the long run, but the number of trades is still too small to determine that along with general strategy profitability. So I’ll press on.

Let's talk about Bond ETFs again. Is that okay?

I'm beating a dead horse here, but I think my old TMF/TMV idea is generally good, and I'm about to put in a twist on it that I should have done when I first published. It's the reason for the top quote.

We already know that for the most part each month, on the last few trading days bonds go up, and on the first few trading days bonds go down. But can’t I make it better? Can I find a new angle?

Pre-hiatus I had made a post about cool and complicated Volatility indices for bonds, and ETF reactions to Futures, and all sorts of nonsense to try and squeeze a big return out of leveraged long-term bond ETFs. So much needless complexity! Why did I not look for the rebalancing effect itself, instead of reaching for 2nd- or 3rd-order indicators of trading strength in similar instruments? A five-year-old-child could have seen the issue. (Future interns will be paid performance bonuses in juice boxes.)

The goal of my TMF/TMV/TLT trade was to front run funds and institutions that were reallocating bonds at the end and beginning of some months because of their internal rebalancing rules or window-dressing. While the returns for going long/short the last/first five trading days of every month were good for TLT itself, I had wanted better. I found the TMF+TMV ETFs and noticed much, much better theoretical returns without the complications of shorting TLT.

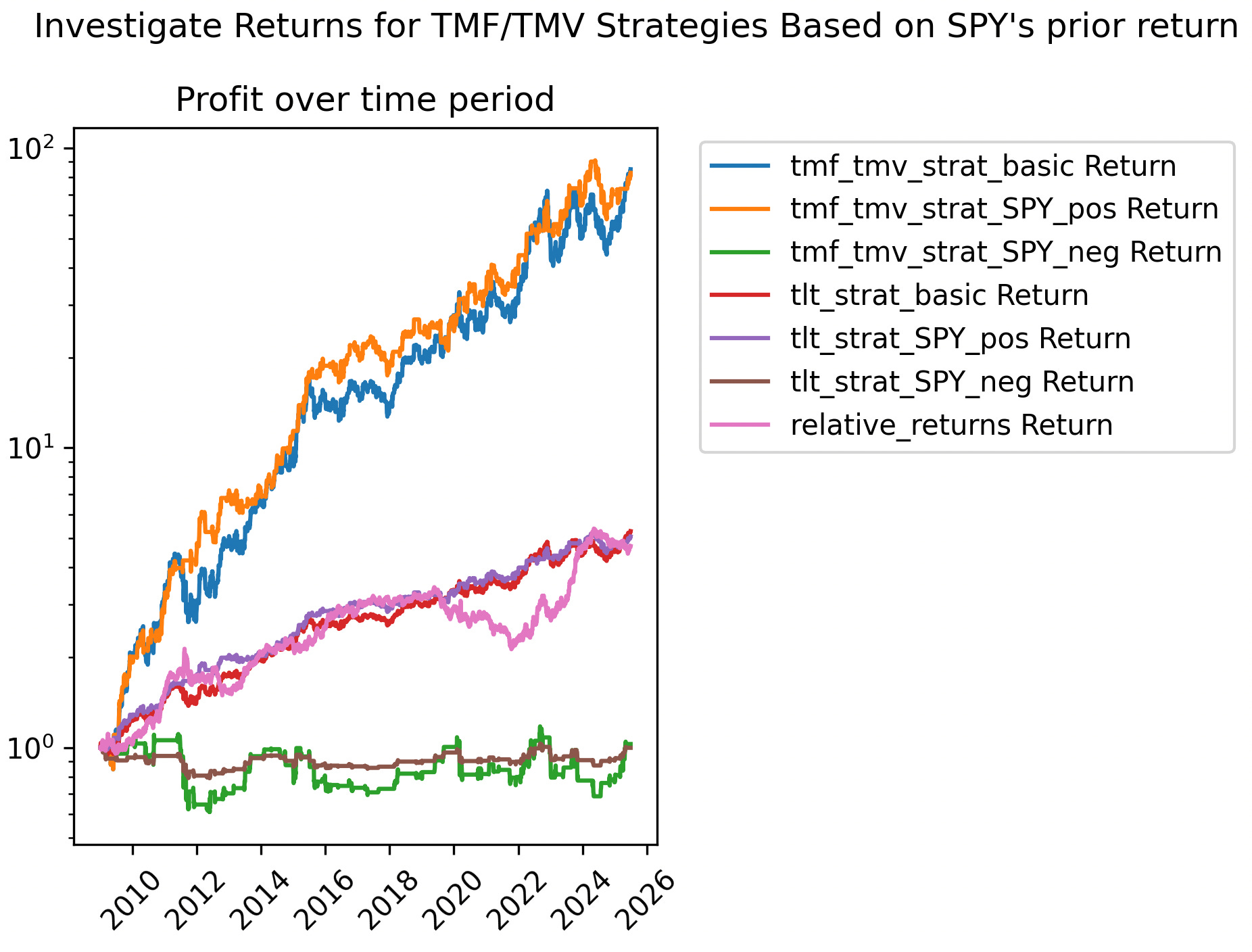

We see yet again that buying and holding TLT, TMF, and TMV on their own don't compare well to SPY’s buy and hold.

But there’s an odd phenomenon the first and last few trading days of a month… Depending on how well the market did. The new simpler rules are such:

When SPY month-to-date returns > 0 at the end of the 6th-to-last trading day for that month, we go long TMF (or long TLT) from the end of the 6th-to-last trading day of the month to the end of the last trading day of the month.

When SPY's 1-month returns > 0 at the end of the last trading day of that month, we go long TMV (or short TLT) from the end of the last trading day of the month, to the end of the fifth day of trading in the next month.

And that’s it. One indicator, one timeframe, ignore everything else.

The SPY itself is a decent measure of ‘the stock market’ and trigger for the strategy. ETFs and Indices like VOO, ^SPX, or VT also work for checking month-to-date and prior-month returns, but SPY is more famous and widespread so we'll use that.

When the trade is filtered by whether the market (SPY) actually went up for the month-to-date or prior month, we see good results with fewer trades enacted.

We see that the returns since 2008 for the TMF/TMV strategy when SPY is positive greatly outclass the strategy investing only when SPY is negative. On a logarithmic scale, we see that the outperformance is rather consistent from 2009 to now. Using the strategy only when SPY's return is positive as indicated in the above rules cuts the amount of time invested by 15% (Instead of being invested ~47% of trading days, the strategy is only invested ~32% of trading days.) Strategy Annualized Return (with risk-free rate set to 0% to be conservative) is still over 30%, with Sharpe and Sortino Ratios > 1. Buy-and-Hold SPY for the entire period only has a 0.83 Sharpe and 1.03 Sortino.

For this trade, slippage should be negligible, since there are at most 2 buys and 2 sells per month of liquid ETFs during a the last few minutes of trading when volume spikes up. This is also a strategy that can be planned days in advance, and shouldn’t require automation or close monitoring. I think it’s a better strategy overall than my first one since I don’t have to check bond futures’ RSI indicators and then maybe switch between TMF and TMV each day over a 10-day period each month.

When fiddling with parameters to test robustness, I found that I don't need to be strict about the decision threshold for SPY's return. A 0%, 1%, or -1% threshold doesn't horribly impact the returns of the positive-SPY TMF/TMV strategy. I haven’t investigated thoroughly, but I believe that SPY is unlikely to move more than a whole percentage point in the minute or two it would take to open a TMF/TMV position near market close.

So as of market close yesterday, I opened a 10% position in TMV in accordance with the modified strategy.

Here is backtest code for the revisited TLT/TMF/TMV strategy.

And in other news, I'm on Twitter now at @lay_quant.

- Lay Quant

Nice post, I have a strat with the same behavior, exploiting EOM patterns but I never thought about using a stock indice filter.

Great analysis!